How you can Assemble a Lengthy-Solely Multifactor Credit score Portfolio?

There exist two commonest methods for setting up multifactor portfolios. The blending method creates single-factor portfolios after which invests proportionally in every to construct a multifactor portfolio. The built-in method combines single-factor alerts right into a multifactor sign after which constructs a multifactor portfolio primarily based on that multifactor sign. Which methodology is best? It’s laborious to inform, and quite a few papers present every technique’s professionals and cons. The latest paper from Joris Blonk and Philip Messow explores this query from the standpoint of the credit score fixed-income portfolio supervisor and provides their evaluation, which reveals that an built-in method might be higher on this specific asset class.

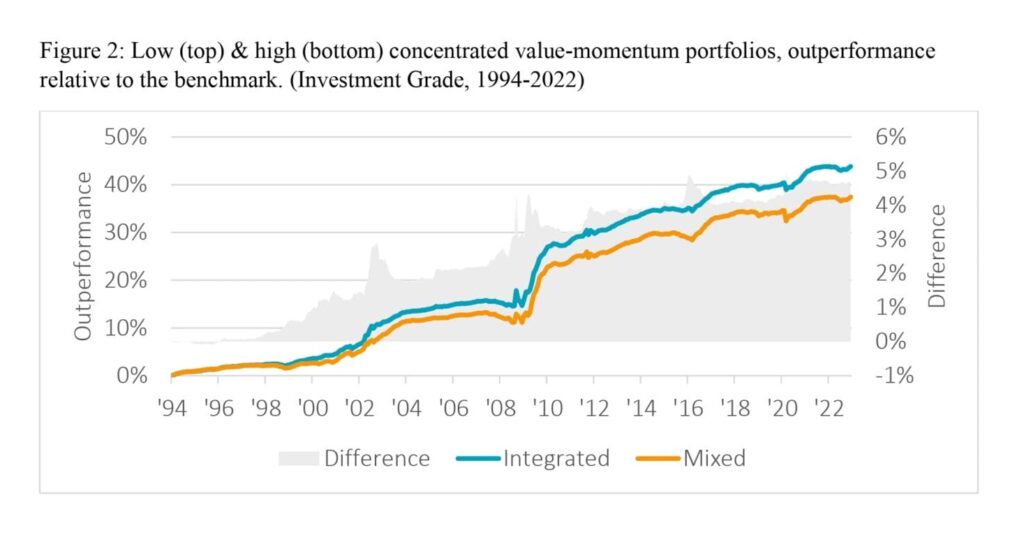

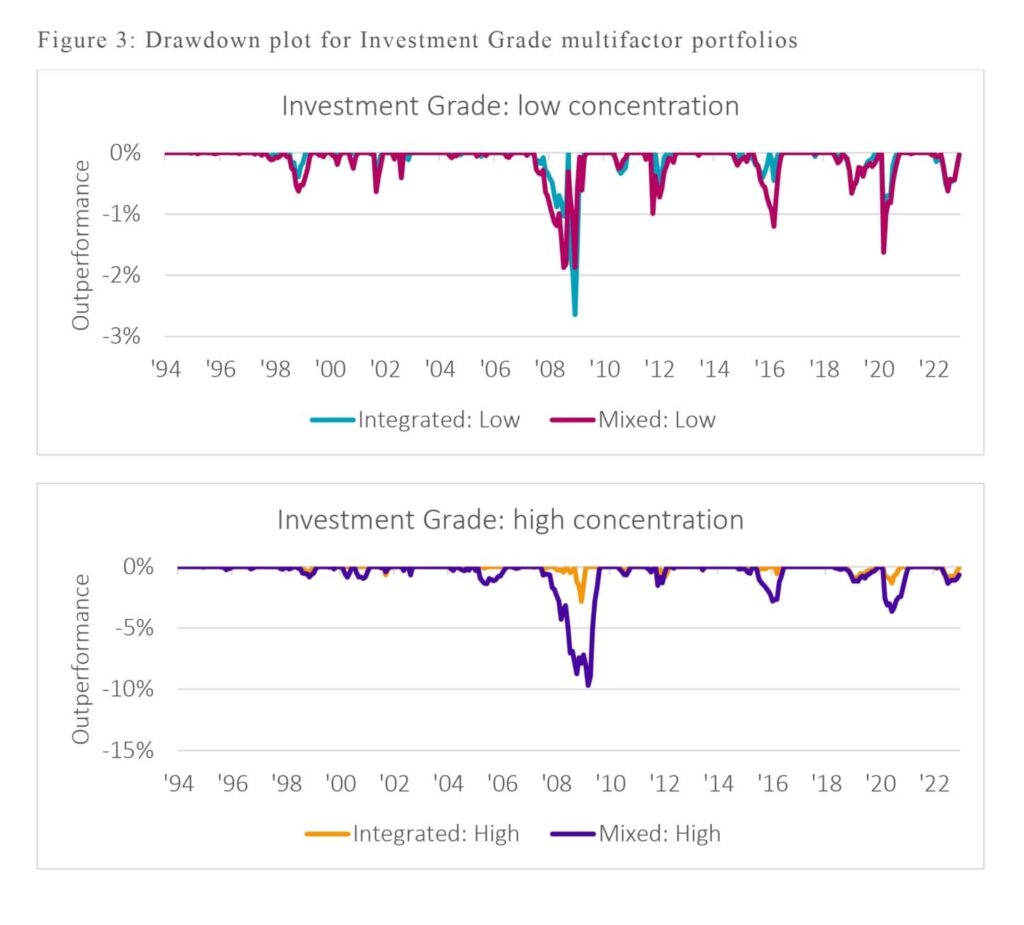

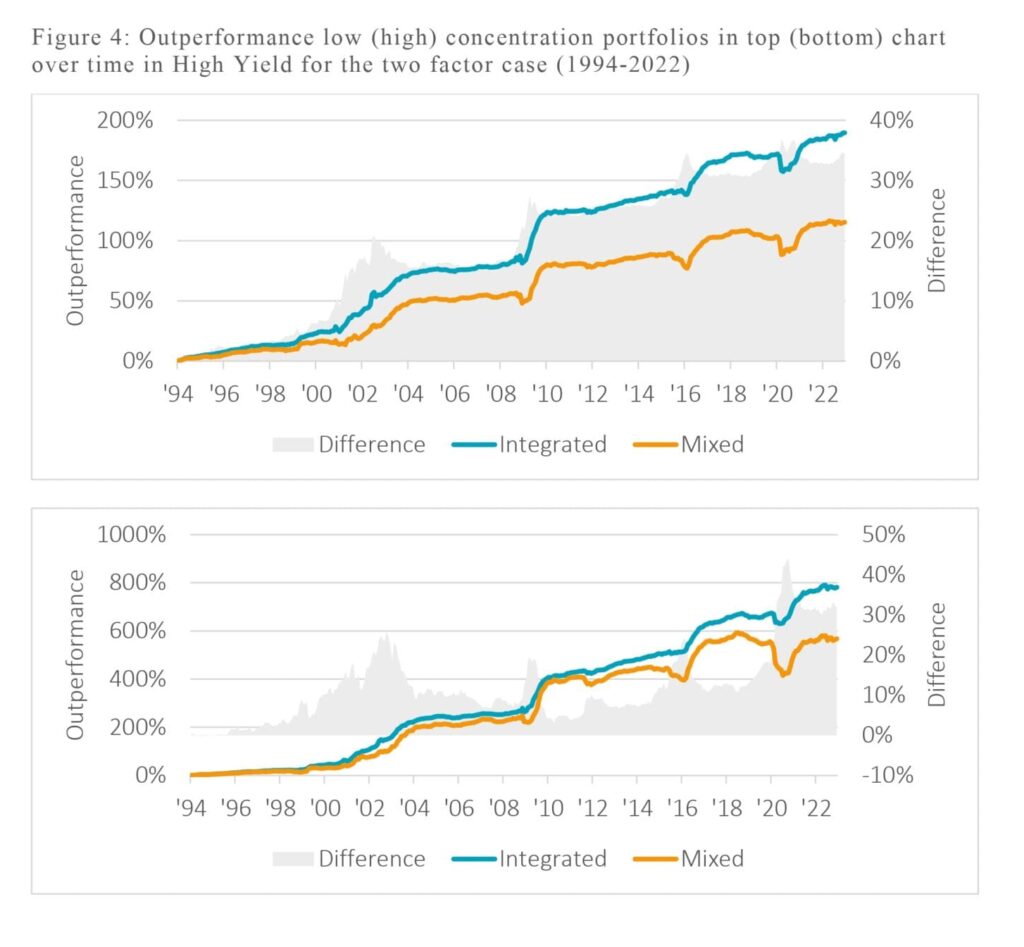

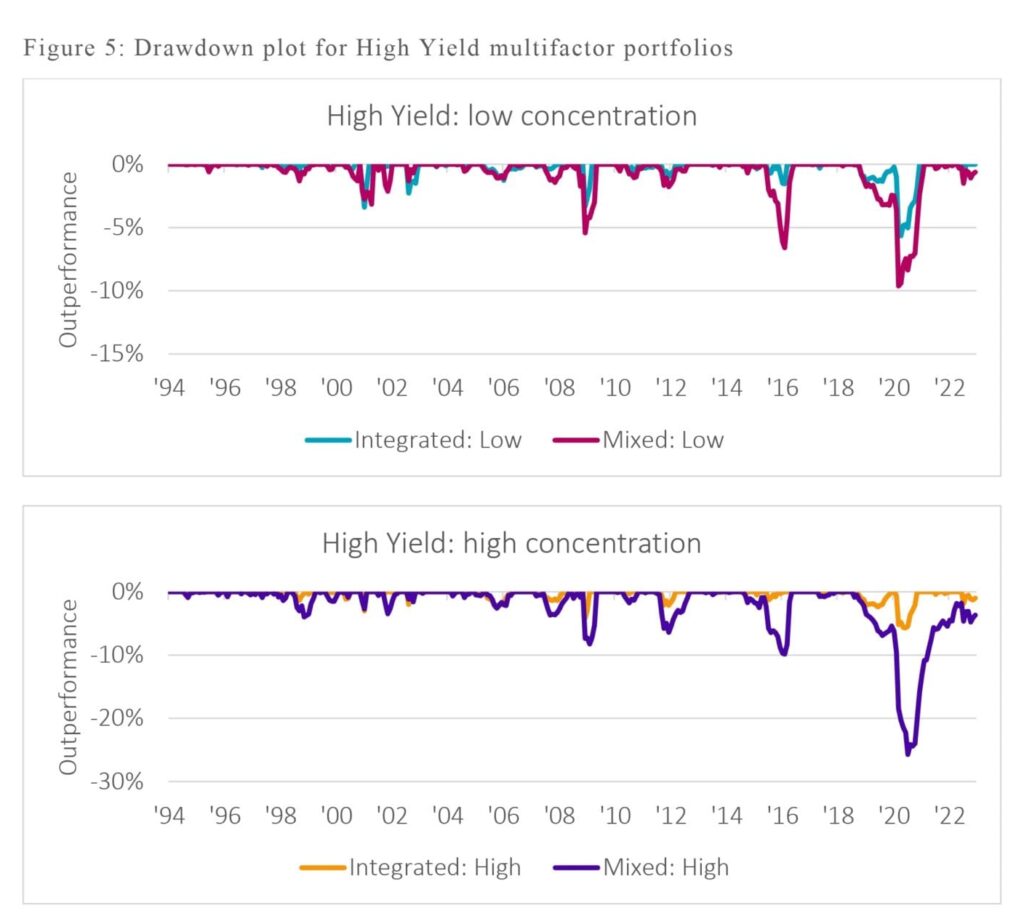

To make these two approaches comparable, authors use exposure-matched portfolios and restrict themselves to long-only portfolios, as long-short methods are extra of a theoretical assemble than a practical, sensible utility for company bond buyers. The authors discovered constant outcomes that indicated that built-in multifactor portfolios outperformed blended multifactor portfolios. These outcomes maintain throughout totally different funding universes (Funding Grade and Excessive Yield), totally different underlying issue suites (two or 4 components), totally different publicity concentrations (low or excessive), and totally different market environments (falling/rising rates of interest, falling/rising credit score spreads, and so forth.).

As well as, they present that an built-in method reduces draw back danger by avoiding investing in bonds with offsetting single-factor exposures (e.g., excessive worth & low momentum), the so-called “worth traps.” Most research within the credit score issue investing literature lack a solution to implementing these methods beneath reasonable circumstances and reaching enticing risk-adjusted returns. Their evaluation gives a primary course for translating these theoretical research into “actual” portfolios. Due to this fact, this research has necessary implications for practitioners who wish to implement multifactor methods for company bonds.

The following logical step can be to ask one other query – which method is best in all-equity funding universe the place shorting is allowed and simpler?

Authors: Joris Blonk and Philip Messow

Title: How you can Assemble a Lengthy-Solely Multifactor Credit score Portfolio?

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4775767

Summary:

This paper examines the best way to mix single components right into a multifactor portfolio of company bonds. The 2 commonest approaches within the literature are the so-called ‘built-in’ and ‘mixing’ approaches. This paper analyzes these two strategies in company bond markets, and finds that the built-in issue portfolios typically result in greater risk-adjusted returns. That is largely as a consequence of the truth that they don’t put money into underperforming bonds that rating poorly on a single issue, to which the ‘mixing’ method is uncovered to. Our outcomes are strong over time and maintain in numerous macro environments and in each Funding Grade and Excessive Yield markets.

As all the time, we current a number of thrilling figures and tables:

Notable quotations from the tutorial analysis paper:

“

“Mixing” requires two steps. Step one is to create portfolios primarily based on the person components, after which to create a blended portfolio from these particular person portfolios by investing proportionately in every of the person issue portfolios.

The “built-in” method requires the development of solely a single portfolio, as the person alerts are first mixed into an total sign and the portfolio is then constructed on the idea of this multifactor sign.

The controversy within the educational literature has targeted totally on the query of which method gives greater risk-adjusted returns. Proponents of built-in multifactor portfolios argue that this method avoids securities with reverse issue loadings (i.e., securities that carry out effectively on one issue however poorly on one other) whereas favoring securities with balanced optimistic exposures to the specified components. This tends to cut back turnover and thus transaction prices, that are significantly necessary within the credit score area.

Nonetheless, there are additionally arguments for mixing. In equities, for instance, research present that there’s little distinction in efficiency between strategies in areas of low monitoring error. Mixing does, nevertheless, facilitate efficiency attribution, because the over- or underperformance of the multifactor portfolio may be immediately attributed to the underlying particular person issue portfolios. This will increase the transparency of the funding method. We look at which of the 2 approaches, built-in or mixing, is extra helpful within the company bond market. There are some distinctive options of the bond market, such because the separation between Funding Grade and Excessive Yield, or the upper implementation prices of lively methods, which can result in totally different outcomes than on the fairness facet. We concentrate on the sensible utility of long-only credit score portfolios, as shorting company bonds is especially difficult as a result of shorting prices are even greater in comparison with equities.”

Are you on the lookout for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to study extra about Quantpedia Premium service? Test how Quantpedia works, our mission and Premium pricing provide.

Do you wish to study extra about Quantpedia Professional service? Test its description, watch movies, evaluation reporting capabilities and go to our pricing provide.

Are you on the lookout for historic information or backtesting platforms? Test our record of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookSeek advice from a pal

Expands Business Drone Use – TradersPro")