Design Selections in ML and the Cross-Part of Inventory Returns

Current developments in machine studying have considerably enhanced the predictive accuracy of inventory returns, leveraging complicated algorithms to research huge datasets and determine patterns that conventional fashions typically miss. The most recent empirical examine by Minghui Chen, Matthias X. Hanauer, and Tobias Kalsbach reveals that design decisions in machine studying fashions, reminiscent of characteristic choice and hyperparameter tuning, are essential to bettering portfolio efficiency. Non-standard errors in machine studying predictions can result in substantial variations in portfolio returns, highlighting the significance of sturdy mannequin analysis methods. Integrating machine studying methods into portfolio administration has proven promising ends in optimizing inventory returns and total portfolio efficiency. Ongoing analysis focuses on refining these fashions for higher monetary outcomes.

Present analysis reveals substantial variations in key design selections, together with algorithm choice, goal variables, characteristic therapies, and coaching processes. This lack of consensus ends in vital final result variations and hinders comparability and replicability. To deal with these challenges, the authors current a scientific framework for evaluating design decisions in machine studying for return prediction. They analyze 1,056 fashions derived from numerous mixtures of analysis design decisions. Their findings reveal that design decisions considerably influence return predictions. The non-standard error from unsuitable decisions is 1.59 instances increased than the usual error.

Key findings embody:

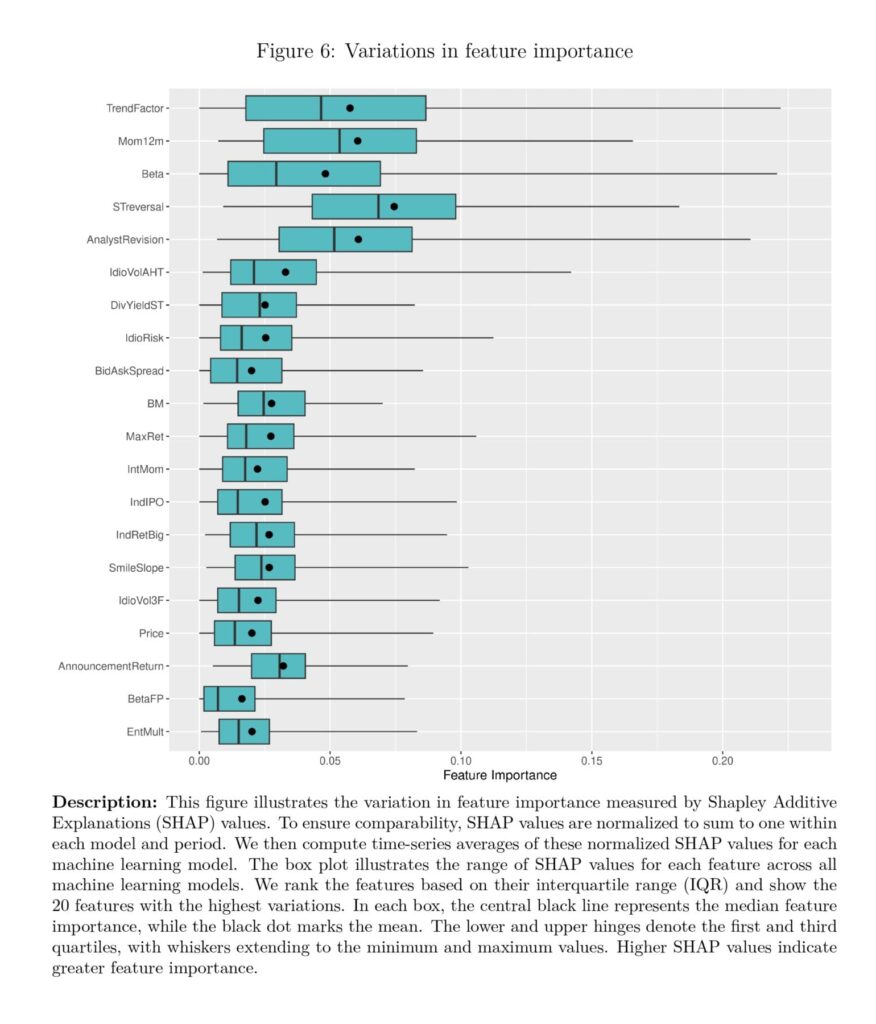

ML returns fluctuate considerably throughout design decisions (see Determine 2 under).

Non-standard errors arising from design decisions exceed customary errors by 59%.

Non-linear fashions are likely to outperform linear fashions just for particular design decisions.

The authors present sensible suggestions within the type of actionable steering for ML mannequin design.

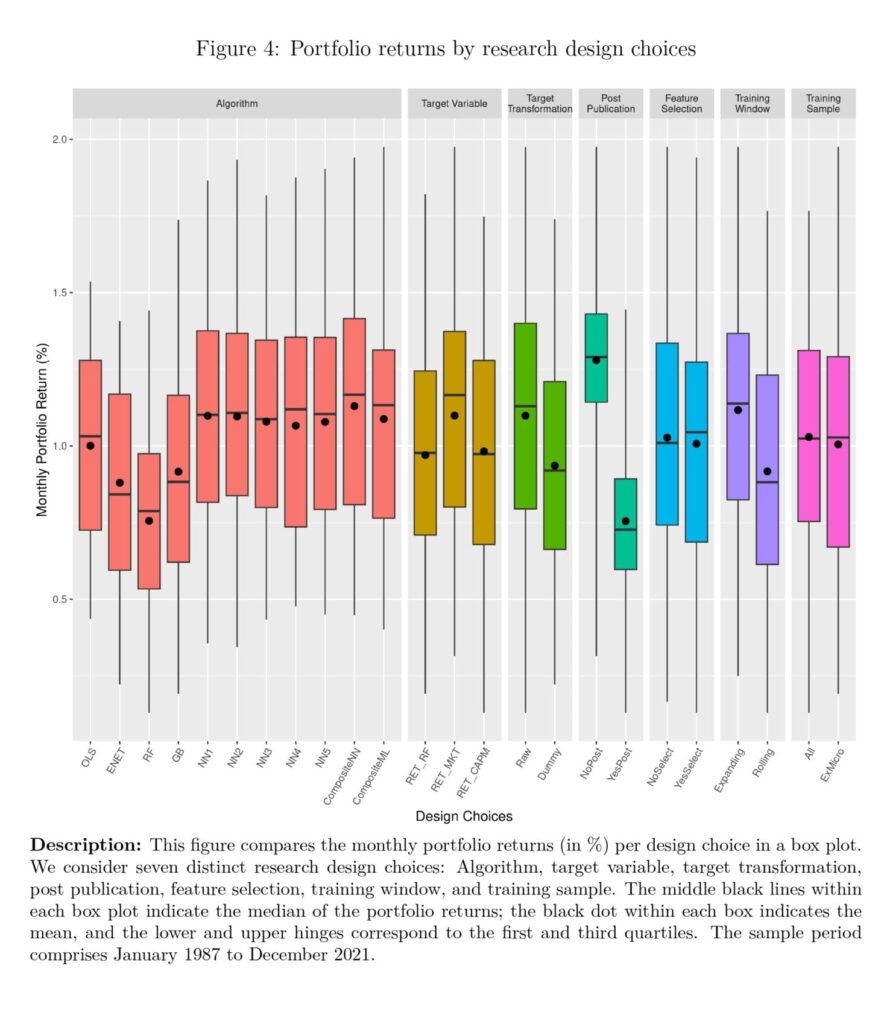

The examine identifies essentially the most influential design decisions affecting portfolio returns. These embody post-publication remedy, coaching window, goal transformation, algorithm, and goal variable. Excluding unpublished options in mannequin coaching decreases month-to-month portfolio returns by 0.52%. An increasing coaching window yields a 0.20% increased month-to-month return than a rolling window.

Moreover, fashions with steady targets and forecast mixtures carry out higher, highlighting the significance of those design decisions. The authors present steering on choosing acceptable selections based mostly on financial results. They suggest utilizing irregular returns relative to the market because the goal variable to attain increased portfolio returns. Non-linear fashions outperform linear OLS fashions below particular situations, reminiscent of steady goal returns or increasing coaching home windows. The examine emphasizes the necessity for cautious consideration and rational justification of analysis design decisions in machine studying.

Authors: Minghui Chen, Matthias X. Hanauer, and Tobias Kalsbach

Title: Design decisions, machine studying, and the cross-section of inventory returns

Hyperlink: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=5031755

Summary:

We match over one thousand machine studying fashions for predicting inventory returns, systematically various design decisions throughout algorithm, goal variable, characteristic choice, and coaching methodology. Our findings display that the non-standard error in portfolio returns arising from these design decisions exceeds the usual error by 59%. Moreover, we observe a considerable variation in mannequin efficiency, with month-to-month imply top-minus-bottom returns starting from 0.13% to 1.98%. These findings underscore the crucial influence of design decisions on machine studying predictions, and we provide suggestions for mannequin design. Lastly, we determine the situations below which non-linear fashions outperform linear fashions.

As all the time, we current a number of bewitching figures and tables:

Notable quotations from the tutorial analysis paper:

“The principle findings of our examine might be summarized as follows: First, we doc substantial variation in top-minus-bottom decile returns throughout completely different machine studying fashions. For instance, month-to-month imply returns vary from 0.13% to 1.98%, with corresponding annualized Sharpe ratios starting from 0.08 to 1.82.Second, we discover that the variation in returns attributable to these design decisions, i.e., the non-standard error, is roughly 1.59 instances increased than the usual error from the statistical bootstrapping course of.

[. . .] we contribute to research that present pointers for finance analysis. As an illustration, Ince and Porter (2006) supply pointers for dealing with worldwide inventory market information, Harvey et al. (2016) suggest the next hurdle for testing the importance of potential components, and Hou et al. (2020) suggest strategies for mitigating the influence of small shares in portfolio types. By providing steering on design decisions for machine learning- based mostly inventory return predictions, we assist scale back uncertainties in mannequin design and improve the interpretability of prediction outcomes.

[. . .] examine has necessary implications for machine studying analysis in finance. A deeper understanding of the crucial design decisions is important for optimizing machine studying fashions, thereby enhancing their reliability and effectiveness in predicting inventory returns. By addressing variations in analysis settings, our work helps researchers demon- strate the robustness of their findings and scale back non-standard errors in future research. This, in flip, permits for extra correct and nuanced interpretations of outcomes.

When predicting inventory returns utilizing machine studying algorithms, researchers and prac- titioners face a variety of necessary methodological decisions. We determine such variations in design decisions in a number of revealed machine-learning research, all of which predict the cross-section of inventory returns. Extra particularly, these research embody Gu et al. (2020), Freyberger et al. (2020), Avramov et al. (2023), and Howard (2024) for U.S. market, Rasekhschaffe and Jones (2019) and Tobek and Hronec (2021) for international developed mar- kets, Hanauer and Kalsbach (2023) for rising markets, and Leippold et al. (2022) for the Chinese language market. In complete, we determine variations in seven frequent analysis design decisions throughout these research, and we categorize them into 4 most important varieties concerning the algorithm, goal, characteristic, and coaching course of. Desk 1 summarizes the particular design decisions of those research.

Subsequent, we examine the efficiency dispersion of the completely different machine-learning strate- gies ensuing from completely different design decisions. Determine 2 reveals the cumulative efficiency of the 1,056 long-short portfolios. Every line represents the efficiency of 1 particular set of analysis design decisions.The determine reveals that the variation in design decisions results in a considerable variation in returns. A hypothetical $1 funding in 1987 results in a last wealth starting from $0.94 (annual compounded return of -0.17%) to $2,652 (annual compounded return of 24.48%) in 2021. The most effective mannequin is related to design decisions of Algorithm (ENS ML), Goal (RET-MKT, RAW), Function (No Submit Publication, No Function Choice), and Coaching (Increasing Window, ExMicro Coaching Pattern). Alternatively, the worst-performing mannequin is related to the design decisions of Algorithm (RF), Goal (RET-CAPM, RAW), Function (Sure Submit Publication, Sure Function Choice), and Coaching (Rolling Window, All Coaching Pattern). The main points of the top- and bottom-performing fashions are documented in Appendix Desk B.2. Other than that, we additionally observe that every one the machine studying fashions carry out worse in recent times, notably after 2004, which aligns with the findings of Blitz et al. (2023).

Determine 4 reveals the portfolio returns in a field plot with the imply, median, first quartile, third quartile, minimal, and most values.The algorithm selection comprises eleven options, comprising linear strategies (OLS, ENET), tree-based strategies (RF and GB), neural networks with one to 5 hidden layers (NN1-NN5), in addition to an ensemble of all neural networks (ENS NN) and an ensemble of all non-linear ML strategies (ENS ML). The outcomes present that the composite strategies exhibit increased imply and median portfolio returns than the opposite 9 particular person algorithms. Whereas our major focus is to not examine particular person algorithms, we discover that the neural networks (NN) show higher efficiency, whereas random forest (RF), on common, performs the worst.”

Are you searching for extra methods to examine? Join our e-newsletter or go to our Weblog or Screener.

Do you wish to study extra about Quantpedia Premium service? Examine how Quantpedia works, our mission and Premium pricing supply.

Do you wish to study extra about Quantpedia Professional service? Examine its description, watch movies, evaluate reporting capabilities and go to our pricing supply.

Are you searching for historic information or backtesting platforms? Examine our record of Algo Buying and selling Reductions.

Or comply with us on:

Fb Group, Fb Web page, Twitter, Linkedin, Medium or Youtube

Share onLinkedInTwitterFacebookConsult with a buddy

Expands Business Drone Use – TradersPro")