")

By Mahavir Bhattacharya

Conditions

To totally grasp the bias-variance tradeoff and its position in buying and selling, it’s important first to construct a powerful basis in arithmetic, machine studying, and programming.

Begin with the basic mathematical ideas mandatory for algorithmic buying and selling by studying Inventory Market Math: Important Ideas for Algorithmic Buying and selling. It will assist you to develop a powerful understanding of algebra, arithmetic, and chance—essential components in statistical modelling.

For the reason that bias-variance tradeoff is intently linked to regression fashions, undergo Exploring Linear Regression Evaluation in Finance and Buying and selling to grasp how regression-based predictive fashions work. To additional strengthen your understanding, Linear Regression: Assumptions and Limitations explains frequent pitfalls in linear regression, that are straight associated to bias and variance points in mannequin efficiency.

Since this weblog focuses on a machine studying idea, it is essential to start out with the fundamentals. Machine Studying Fundamentals: Parts, Utility, Assets, and Extra introduces the basic features of ML, adopted by Machine Studying for Algorithmic Buying and selling in Python: A Full Information, which demonstrates how ML fashions are utilized in monetary markets.When you’re new to Python, begin with Fundamentals of Python Programming. Moreover, the Python for Buying and selling: Primary free course gives a structured method to studying Python for monetary information evaluation and buying and selling methods.

This weblog covers:

Ice Breaker

Machine studying mannequin creation is a tightrope stroll. You create a straightforward mannequin, and you find yourself with an underfit. Improve the complexity, and you find yourself with an overfitted mannequin. What to do then? Properly, that’s the agenda for this weblog publish. That is the primary a part of a two-blog sequence on bias-variance tradeoff and its use in market buying and selling. We’ll discover the basic ideas on this first half and talk about the appliance within the second half.

Producing Random Values with a Uniform Distribution and Becoming Them to a Second-Order Equation

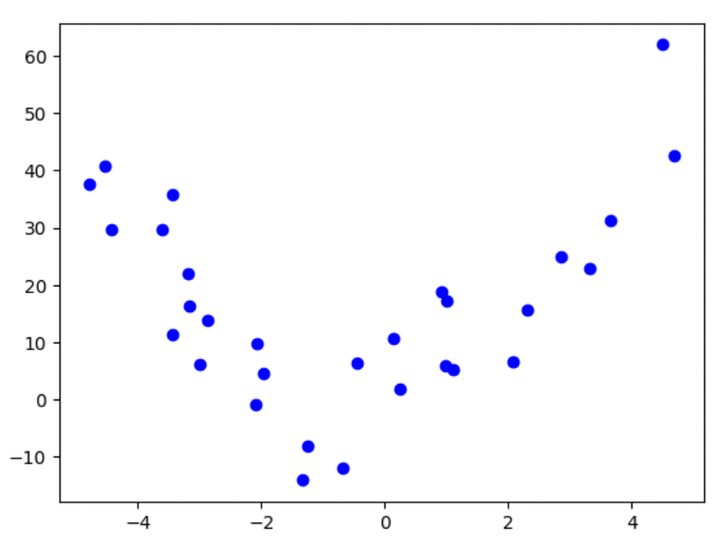

Let’s begin with a easy illustration of underfitting and overfitting. Let’s take an equation and plot it. The equation is:

$$y = 2X^2 + 3X + 4$$

When plotted, that is the way it appears to be like like:

Determine 1: Plot of the second-order polynomial

Right here’s the Python code for plotting the equation:

I’ve assigned random values to X, which vary from -5 to five and belong to a uniform distribution. Suppose we’re given solely this scatter plot (not the equation). With some primary math data, we may determine it as a second-order polynomial. We will even do that visually.

However in actual settings, issues aren’t that easy. Any information we collect or analyze won’t type such a transparent sample, and there shall be a random element. We time period this random element as noise. To know extra about noise, you possibly can undergo this weblog article and in addition this one.

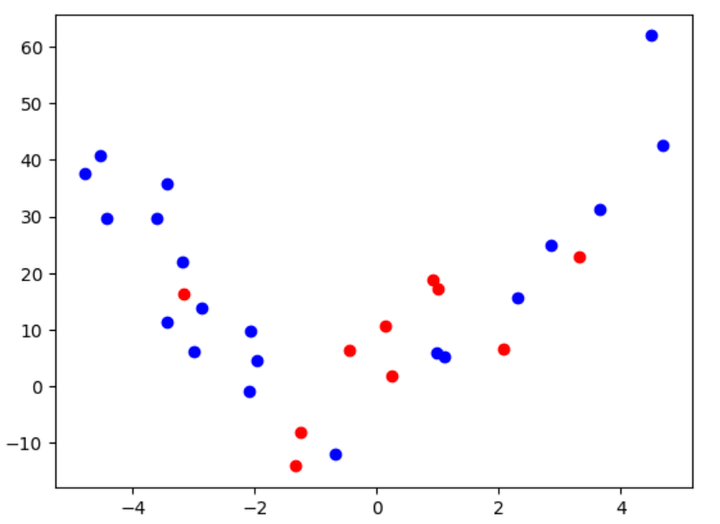

Including a Noise Part

Once we add a noise element to the above equation, that is the way it appears to be like like:

$$y = 2X^2 + 3X + 4 + noise$$

What would its plot appear like? Right here you go:

Determine 2: Plot of the second-order polynomial with noise

Do you suppose it’s as simply interpretable because the earlier one? Possibly, since we solely have 30 information factors, the curve nonetheless appears to be like considerably second-orderish! However we’ll want a deeper evaluation when we now have many information factors, and the underlying equation additionally begins getting extra complicated.

Right here’s the code for producing the above information factors and the plot from Determine 2:

Trying intently, you’ll notice that the noise element above belongs to a traditional distribution, with imply = 0 and customary deviation = 10.

Splitting into Testing and Coaching Units

Let’s now talk about the meaty half. We will break up the above information into practice and check units, with sizes of 20 and 10, respectively. When you aren’t conversant with these primary machine-learning ideas, I like to recommend skimming by way of this free e book: ML for Buying and selling.

That is what the information appears to be like like after splitting:

Determine 3: Plot of the second-order polynomial after splitting into practice and check information

Right here’s the code for the break up and the above plot:

Becoming 4 Completely different Fashions to the Information for Illustrating Bias and Variance

After splitting the information, we’ll practice 4 completely different fashions with polynomials of order 1, 2, 3, and 10, respectively, and verify their accuracies. We’ll do that by utilizing linear regression. We’ll import the “PolynomialFeatures” and “LinearRegression” functionalities from completely different sub-modules of the scikit-learn library. Let’s see what the 4 fashions appear like after we match them on the information, with their respective accuracies:

Determine 4a: Underfit mannequin with excessive bias

Determine 4b: Correctly match mannequin with low bias and low variance (second order)

Determine 4c: Correctly match mannequin with low bias and low variance (third order)

Determine 4d: Overfit mannequin with excessive variance

The above 4 plots (Determine 4a to Determine 4d) ought to provide you with a transparent image of what it appears to be like like when a machine studying mannequin underfits, correctly matches, and overfits on the coaching information. You may marvel why I’m exhibiting you two plots (and thus two completely different fashions) for a correct match. Don’t fear; I’ll talk about this in a few minutes.

For now, right here’s the code for coaching the 4 fashions and for plotting them:

Formal Dialogue on Bias and Variance

Let’s perceive underfitting and overfitting higher now.

Underfitting can also be termed as “bias”. An underfit mannequin doesn’t align with many factors within the coaching information and carries by itself path. It doesn’t enable the information factors to change itself a lot. You’ll be able to consider an underfit mannequin as an individual with a thoughts that’s principally, if not wholly, closed to the concepts, strategies, and opinions of others and at all times carries a psychological bias towards issues. An underfit mannequin, or a mannequin with excessive bias, is simplistic and may’t seize a lot essence or inherent data within the coaching information. Thus, it can’t generalize nicely to the testing (unseen) information. Each the coaching and testing accuracies of such a mannequin are low.

Overfitting is known as “variance”. On this case, the mannequin aligns itself with most, if not all, information factors within the coaching set. You’ll be able to consider a mannequin which overfits as a fickle-minded one that at all times sways on the opinions and choices of others, and doesn’t have any conviction of hertheir personal. An overfit mannequin, or a mannequin with a excessive variance, tries to seize each minute element of the coaching information, together with the noise, a lot in order that it will possibly’t generalize to the testing (unseen) information. Within the case of a mannequin with an overfit, the coaching accuracy is excessive, however the testing accuracy is low.

Within the case of a correctly match mannequin, we get low errors on each the coaching and testing information. For the given instance, since we already know the equation to be a second-order polynomial, we should always anticipate a second-order polynomial to yield the minimal testing and coaching errors. Nevertheless, as you possibly can see from the above outcomes, the third-order polynomial mannequin offers fewer errors on the coaching and the testing information. What’s the explanation for this? Keep in mind the noise time period? Yup, that’s the first cause for this discrepancy. What’s the secondary cause, then? The low variety of information factors!

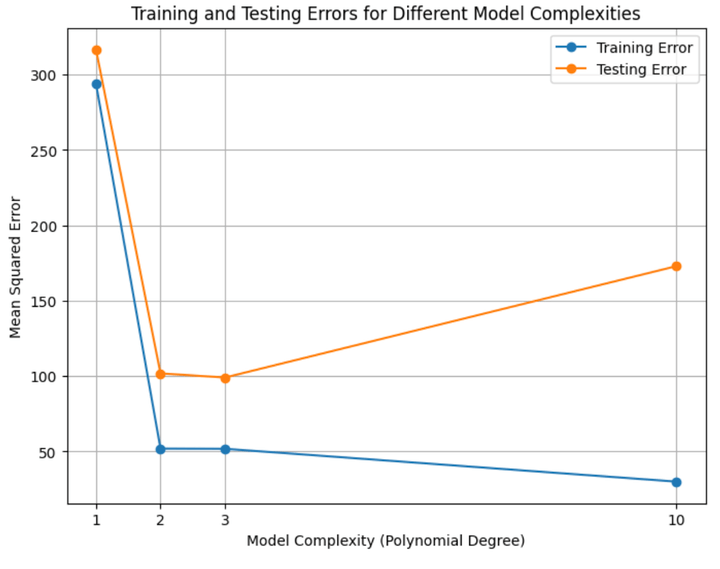

Change in Coaching and Testing Accuracy with Mannequin Complexity

Let’s plot the coaching and testing accuracies of all 4 fashions:

Determine 5: Coaching and testing errors for all of the 4 fashions

From Determine 5 above, we are able to infer the next:

The coaching and testing errors are fairly excessive for the underfit mannequin.The coaching and testing errors are across the lowest for the right match mannequin/s.The coaching error is low (even decrease than the right match fashions), however the testing error is excessive.The testing error is larger than the coaching error in all circumstances.

Oh, and sure, right here’s the code for the above calculation and the plots:

Mathematical Therapy of Completely different Error Phrases and Decomposition

Now, with that out of the way in which, let’s proceed in direction of extra mathematical definitions of bias and variance.

Let’s start with the loss perform. In machine studying parlance, the loss perform is the perform that we need to reduce. Solely after we get the least potential worth of the loss perform can we are saying that we now have educated or match the mannequin nicely.

The imply sq. error (MSE) is one such loss perform. When you’re accustomed to the MSE, you’ll know that the decrease the MSE, the extra correct the mannequin.

The equation for the MSE is:

Thus,

$$MSE = Bias^2 + Variance$$

From the above equation, it’s obvious that to cut back the error, we have to scale back both or each from bias and variance. Nevertheless, since decreasing both of those results in an increase within the different, we have to develop a mix of each, which yields the minimal worth for the MSE. So, if we do this and are fortunate, can we find yourself with an MSE worth of 0? Properly, not fairly! Other than the bias and variance phrases, there’s one other time period that we have to add right here. Owing to the inherent nature of any noticed/recorded information, there may be some noise in it, which includes that a part of the error we will not scale back. We time period this half because the irreducible error. Thus, the equation for MSE turns into:

$$MSE = Bias^2 + Variance + Irreducible;Error$$

Let’s develop an instinct utilizing the identical simulated dataset as earlier than.

We will tweak the equation for MSE:

$$MSE = E[(hat{y} – E[y])^2]$$

How and why did we do that? To get into the main points, confer with Neural Networks and the Bias/Variance Dilemma” by Stuart German.

Foundation the above paper, the equation for the MSE is:

$$MSE = E_D[(f(x; D) – E[y|x])^2]$$

the place,

$$D;is;the;coaching;information,$$

$$E_D;is;the;anticipated;worth;with;respect;to;the;coaching;information,$$

$$f(x; D);is;the;perform;of;x,;however;with;dependency;on;the;coaching;information,;and,$$

$$E[y|x];is;the;the;anticipated;worth;of;y;when;x;is;identified.$$

Thus, the bias for every information level is the distinction between the imply of all predicted values and the imply of all noticed values. Fairly intuitively, the lesser this distinction, the lesser the bias, and the extra correct the mannequin. However is it actually so? Let’s not overlook that we enhance the variance after we acquire a match with a low bias.. How will we outline the variance in mathematical phrases? Here is the equation:

$$Variance = E[(hat{y} – E[hat{y}])^2]$$

The MSE includes the above-defined bias and variance phrases. Nevertheless, for the reason that MSE and variance phrases are primarily squares of the variations between completely different y values, we should do the identical to the bias time period to make sure dimensional homogeneity.

Thus,

$$MSE = Bias^2 + Variance$$

From the above equation, it’s obvious that to cut back the error, we have to scale back both or each from bias and variance. Nevertheless, since decreasing both of those results in an increase within the different, we have to develop a mix of each, which yields the minimal worth for the MSE. So, if we do this and are fortunate, can we find yourself with an MSE worth of 0? Properly, not fairly! Other than the bias and variance phrases, there’s one other time period that we have to add right here. Owing to the inherent nature of any noticed/recorded information, there may be some noise in it, which includes that a part of the error we will not scale back. We time period this half because the irreducible error. Thus, the equation for MSE turns into:

$$MSE = Bias^2 + Variance + Irreducible;Error$$

Let’s develop an instinct utilizing the identical simulated dataset as earlier than.

We will tweak the equation for MSE:

$$MSE = E[(hat{y} – E[y])^2]$$

How and why did we do that? To get into the main points, confer with Neural Networks and the Bias/Variance Dilemma” by Stuart German.

Foundation the above paper, the equation for the MSE is:

$$MSE = E_D[(f(x: D) – E[y|x])^2]$$

the place,

$$D;is;the;coaching;information,$$

$$E_D;is;the;anticipated;worth;with;respect;to;the;coaching;information,$$

$$f(x: D);is;the;perform;of;x,;however;with;dependency;on;the;coaching;information,;and,$$

$$E[y|x];is;the;the;anticipated;worth;of;y;when;x;is;identified.$$

We gained’t talk about something extra right here since it’s outdoors the scope of this weblog article. You’ll be able to confer with the paper cited above for a deeper understanding.

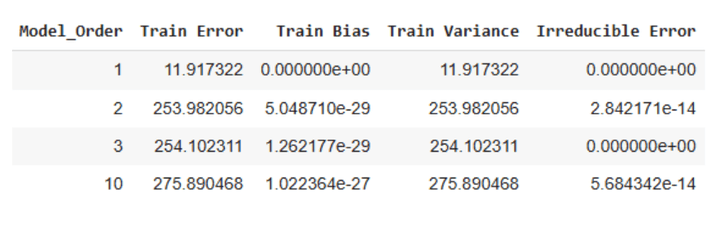

Values of the MSE, Bias, Variance, and Irreducible Error for the Simulated Information, and Their Instinct

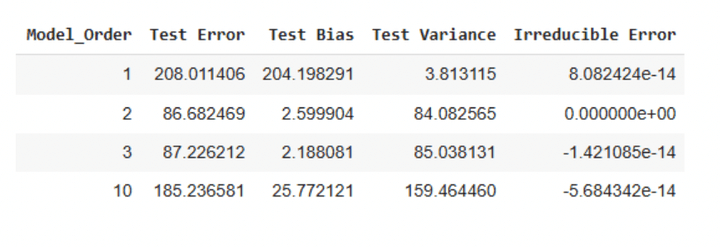

We’ll additionally calculate the bias time period and the variance time period together with the MSE (utilizing the tweaked formulation talked about above).. That is what the values appear like for the testing information:

Desk 1: Testing errors for simulated information

We will make the next observations from Desk 1 above:

The check errors are minimal for fashions with orders 2 and three.The mannequin with order 0 has the utmost bias time period.The mannequin with order 10 has the utmost variance time period.The irreducible error is both 0 or negligible.

Listed below are the corresponding values for the coaching dataset:

Desk 2: Coaching errors for simulated information

We will make the next observations from Desk 2 above:

The coaching errors are larger for the three larger order fashions than the testing errors.The bias time period is negligible for all 4 fashions.The error will increase with rising mannequin complexity.

The above three discrepancies might be attributed to our information comprising solely 20 practice and 10 check information factors. How, regardless of this information sampling, did we not get discrepancies within the check information error calculations? Properly, for one, the check information stays unseen by the mannequin, and the mannequin tried to foretell values based mostly on what it discovered in the course of the coaching. Secondly, there may be an inherent randomness after we work with such small samples, and we could have landed on the luckier facet of issues with the testing information. Thirdly, we did get a discrepancy, with the irreducible errors being virtually 0 within the testing pattern. Like I discussed above, there may be at all times an irreducible error owing to the inherent nature of any information. Nevertheless, we bought no such error since we used information that was simulated by utilizing equations and didn’t use precise noticed information.

The purpose of the above dialogue is to not examine the values that we bought however to derive an instinct of the bias and variance phrases. Hope you will have a transparent image of those phrases now. There’s one other time period referred to as ‘decomposition’. It merely refers to the truth that we are able to ‘decompose’ the overall error of any mannequin into its error owing to bias, error owing to variance, and the inherent irreducible error.

Right here’s the code for getting the above tables:

Until Subsequent Time

Phew! That was quite a bit! We should always cease right here for now. Within the second half, we’ll discover the way to predict market costs and construct buying and selling methods by using bias-variance decomposition.

Subsequent steps

After you have constructed a strong basis, you possibly can discover extra superior purposes of machine studying and regression in buying and selling.

For these trying to improve their Python expertise, Python for Buying and selling by Multi Commodity Trade gives deeper insights into information dealing with, monetary evaluation, and technique implementation utilizing Python.

In case you are focused on machine studying purposes in buying and selling, think about Machine Studying & Deep Studying in Buying and selling. This studying monitor covers key features of ML, from information preprocessing and predictive modeling to AI mannequin optimization, serving to you implement classification and regression methods in monetary markets.

To take your regression-based buying and selling methods additional, Buying and selling with Machine Studying: Regression is a superb useful resource. This course walks you thru the step-by-step implementation of regression fashions for buying and selling, together with information acquisition, mannequin coaching, testing, and prediction of inventory costs.

For a structured method to quantitative buying and selling and machine studying, think about The Govt Programme in Algorithmic Buying and selling (EPAT). This program covers classical ML algorithms (SVM, k-means clustering, choice timber, and random forests), deep studying fundamentals (neural networks and gradient descent), and Python-based technique growth. You’ll additionally discover statistical arbitrage utilizing PCA, different information sources, and reinforcement studying for buying and selling.

As soon as you’ve got mastered these ideas, apply your data in real-world buying and selling utilizing Blueshift, Blueshift is an all-in-one automated buying and selling platform that brings institutional-class infrastructure for funding analysis, backtesting, and algorithmic buying and selling to everybody, wherever and anytime. It’s quick, versatile, and dependable. It’s also asset-class and trading-style agnostic. Blueshift helps you flip your concepts into investment-worthy alternatives.

File within the obtain:

Bias Variance Decomposition – Python pocket book

Be at liberty to make adjustments to the code as per your consolation.

Login to Obtain

All investments and buying and selling within the inventory market contain danger. Any choice to put trades within the monetary markets, together with buying and selling in inventory or choices or different monetary devices is a private choice that ought to solely be made after thorough analysis, together with a private danger and monetary evaluation and the engagement {of professional} help to the extent you consider mandatory. The buying and selling methods or associated data talked about on this article is for informational functions solely.