FinkAvenue

Microsoft (NASDAQ:MSFT) is about to report its fiscal fourth-quarter outcomes, amid an ongoing big-tech and AI selloff.

This Tuesday, Satya Nadella may have an opportunity to reignite AI enthusiasm, as issues about near-term monetization proceed to rise.

In an all-important report, Microsoft will present an preliminary look into its subsequent fiscal yr, in addition to make clear different key enterprise strains like Workplace, LinkedIn, Gaming, and {Hardware}.

Let’s dive in.

Cautious Setup Into The Print

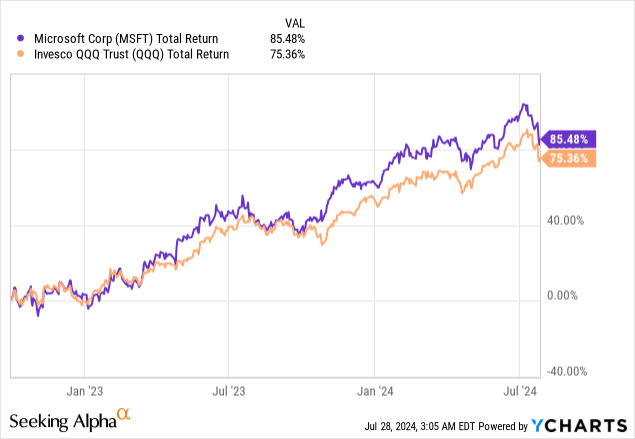

I have been masking Microsoft on In search of Alpha since Could of final yr, a number of months into the good rebound of 2023.

For the reason that backside of October 2022, Microsoft, and the remainder of huge tech, have all seen their shares go up and to the fitting, fairly easily.

There have been actually solely three hiccups alongside the best way. In October 2023 and April 2024, the downturns have been primarily a results of a altering macro outlook, as price expectations responded to inflation issues.

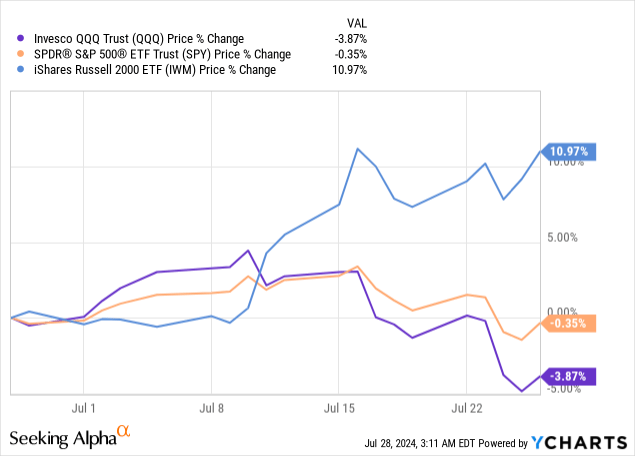

Nevertheless, this time, the alternative is true. As price cuts develop into more and more sure, the market appears desperate to reallocate funds to riskier, extra interest-sensitive corporations (i.e. small caps).

As well as, and maybe extra related to the aim of this text, AI enthusiasm is fading. Whereas there appears to be a consensus of optimism relating to AI’s potential to develop into a serious paradigm shift, there’s rising suspicion concerning the astounding quantities of capital investments by huge tech.

Consequently, Microsoft is as soon as once more coming right into a report with a considerably handy setup, because it will get the possibility to reignite investor confidence.

Let’s dive into the important thing components to watch which is able to drive the shares within the near-to-mid-term.

Azure, AI Contribution, And The 31% Threshold

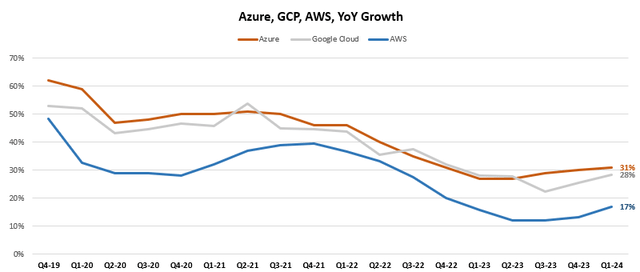

Since calendar Q3’23, Azure has taken again the lead in cloud progress within the three-horse race with Amazon’s (AMZN) AWS and Alphabet’s (GOOG) GCP.

Created and calculated by the writer utilizing knowledge from the businesses’ monetary experiences; Microsoft’s fiscal quarter is 2 durations forward of the calendar yr, that means Q1-24 is Microsoft’s fiscal Q3-24.

Not coincidentally, this was proper round when AI grew to become a giant resolution issue, and Open AI, which is obtainable solely by Azure, took the world by storm.

Notably, among the many three hyper scalers, Microsoft is the one one who quantified AI’s contribution to its progress, coming in at 7 factors final quarter.

Azure maintained a ~30% progress price for 3 consecutive quarters, and it is anticipated to come back above that, at 31%, on this upcoming quarter. Channel checks are aligned on a beat, and there isn’t any motive to anticipate lower than 31% progress.

On the final earnings name, Microsoft mentioned that regardless that progress is accelerating, it was nonetheless supply-constrained, and I am positive it will be requested to offer an replace on that entrance. If Azure comes at 31% and administration reiterates a scarcity of provide, this will likely be an excellent signal.

It is also value noting that the non-AI progress alternative stays enormous, as a bit of over 50% of workloads are nonetheless achieved on-prem.

So, What Are Buyers So Involved About?

First, open supply. Meta (META) is making waves throughout the business with its open Llama mannequin, which appears to be on par with the main closed fashions. This raises huge questions concerning the validity of closed LLMs as a enterprise. Though Microsoft itself provides Llama by Azure, the corporate’s enormous investments in OpenAI may not be as profitable as initially thought.

Second, clients’ ROI. In contrast to most of its clients, Microsoft is already monetizing AI, primarily by Azure and Copilots. Virtually each tech firm is doing one thing in AI, however not a lot of them have come out with true AI-based merchandise.

I feel there’s far more innovation and success on that entrance than what AI bears declare. Nevertheless, it is nonetheless very early.

Workplace, Copilots

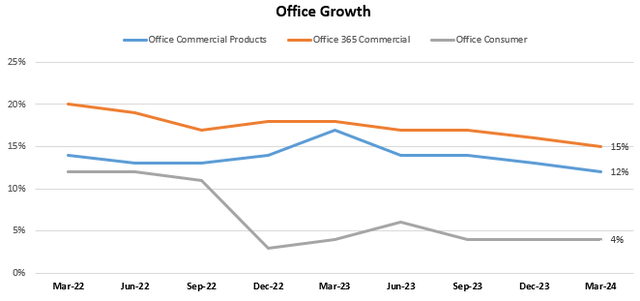

Workplace stays arguably the strongest software program enterprise on the planet, and regardless of a number of a long time of management, Microsoft continues to be innovating and gaining market share, sustaining double-digit progress within the enterprise segments.

Created by the writer based mostly on knowledge from Microsoft monetary experiences.

Microsoft’s personal end-point AI product is its copilots. Thus far, the first use case is GitHub copilot, with 1.8 million paid subscribers, rising 35% QoQ. At a value degree of $21 per person per 30 days, that is a direct $500 million run price. Not too important for a corporation as huge as Microsoft, however nonetheless spectacular.

As well as, Microsoft is seeing continued adoption of its Workplace Copilots, in addition to its Copilot Studio. They nonetheless anticipate this to develop into their quickest product to achieve $10 billion.

Workplace 365 Business is anticipated to develop 14%, Workplace Shopper low-to-mid-single-digits, and Workplace on-prem, is anticipated to say no, as migrations to the cloud proceed.

Gadgets, Home windows & Safety

I made a decision to pile these three collectively as a result of I feel they’re generally underappreciated by the market, for varied causes, and I anticipate all three of them to develop into a significant progress driver within the close to time period.

Safety

First, safety. Microsoft has a $20 billion safety enterprise throughout a number of segments. Safety is likely one of the fastest-growing classes in tech, and it is solely accelerating. With rising geopolitical pressure, it looks like each day there is a new cyberattack, and it is affecting key mission-critical sectors of the economic system together with healthcare and telecom.

I am unsure why Microsoft would not get away extra particulars about its safety merchandise, however it’s completely positioned to develop into the world’s largest cybersecurity firm within the cloud, with its unparalleled penetration in enterprise clients.

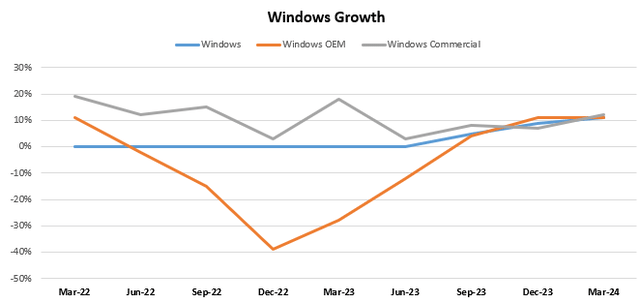

Home windows

Second, Home windows. Home windows has been a drag on Microsoft’s outcomes all all through fiscal 2023, nevertheless it turned optimistic beginning Q1’24, which resulted in September 2023.

Created by the writer based mostly on knowledge from Microsoft monetary experiences.

Home windows progress accelerated for 3 consecutive quarters and is anticipated to decelerate within the upcoming quarter. Nevertheless, it needs to be famous that this quarter’s comps are simpler, and I anticipate a beat.

Gadgets

Gadgets income progress has been unfavorable for six consecutive quarters, pushed by the Covid pull-forward impact. We’re seeing the identical development throughout different main machine suppliers, together with the chief Apple (AAPL).

Regardless of AI capabilities probably driving an improve cycle, Gadgets are nonetheless anticipated to say no within the mid-teens this quarter.

Nevertheless, this quarter is not as essential because the information for the subsequent quarter, which is able to embrace the Copilot+ PCs. With the assistance of handy comps, I am anticipating a a lot better information for subsequent quarter.

Gaming

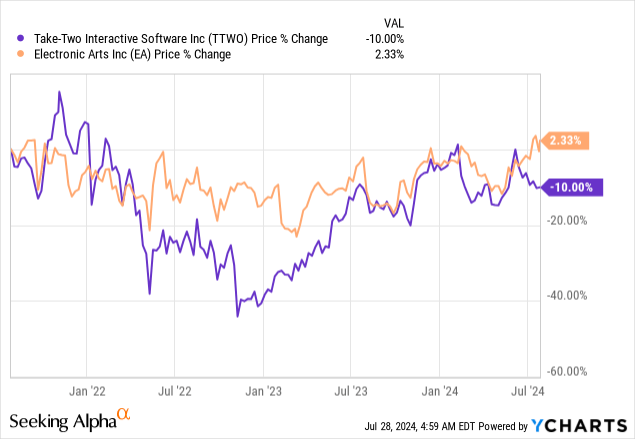

Microsoft’s gaming division has now develop into the Activision phase in essence, because it’s the most important element of the enterprise. Considerably below the radar and neglected by traders, I feel that Microsoft is failing in gaming, and the Activision acquisition would have been far more scrutinized if gaming wasn’t a not-so-important phase in Microsoft.

All the gaming business is struggling proper now, as mirrored by the 3-year efficiency of Take-Two (TTWO) and Digital Arts (EA).

{Hardware} gross sales are plunging, and triple-A video games have gotten more and more costly to develop. That is one other business that is struggling to recuperate from the pull-forward impact of COVID-19, along with the truth that cellular video games are taking share and community-based video games like Fortnite and Roblox are taking a lot of the engagement.

Nonetheless, gaming is a large business, and any signal of enchancment on that entrance can be nice for the inventory.

Promoting, LinkedIn & Bing

Eventually, we get to Microsoft’s web companies, in LinkedIn and Bing. Each are primarily promoting platforms, though LinkedIn has a really robust subscription enterprise in LinkedIn Premium.

These are two extremely worthwhile companies, which have been accelerating over the previous a number of quarters.

For Search, it was primarily market share positive factors pushed by AI innovation in Bing.

For LinkedIn, it has been a product innovation story, as the corporate is capturing extra enterprise and including worth to clients amid a harder job market.

Search is anticipated to speed up from 12% to mid-teens progress, whereas LinkedIn is anticipated to decelerate from 9% to mid-to-high-single digits.

Valuation & Steerage

I feel it is truthful to say we established Microsoft as a particularly diversified enterprise, with extraordinary progress prospects in each single one in all them, and clear business management in most.

Three components will drive share efficiency following this report. One, beating this quarter’s expectations as we mentioned. Two, offering optimistic steering for the subsequent quarter, in addition to optimistic commentary for subsequent yr, which they already mentioned needs to be one other yr of double-digit income and working earnings progress.

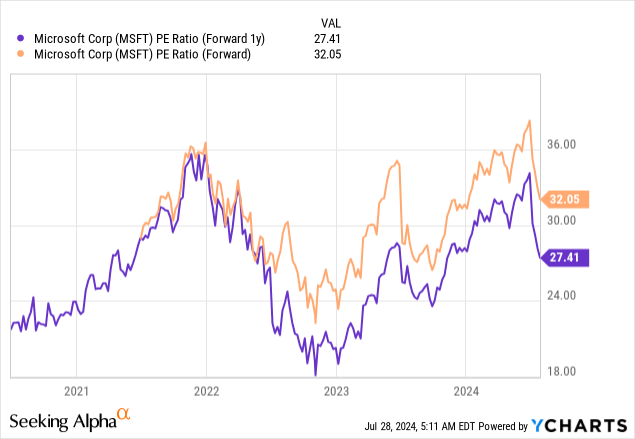

Three, valuation.

It is humorous how this stuff work, however in three days, Microsoft will not be buying and selling at 36 instances ahead earnings, however relatively at a 32x a number of, as shares will begin buying and selling based mostly on the corporate’s FY25 numbers.

That places Microsoft consistent with its historic common. Frankly, not screaming engaging.

Nevertheless, I nonetheless imagine that is a lovely entry level. Microsoft is anticipated to develop EPS at a mid-teens tempo for the foreseeable future and shopping for shares at a good valuation is sufficient to generate market-beating returns.

As well as, Microsoft all the time beats expectations and FY25 needs to be no exception, that means it is really barely undervalued.

Lastly, Microsoft is arguably greatest positioned to capitalize on AI, with the bottom danger of overspending because of its unparalleled demand alerts and best-of-breed administration. With that in thoughts, I feel a premium over historic valuation can be cheap.

Conclusion

Microsoft is about to report its outcomes for the final quarter of its fiscal yr this Tuesday.

As soon as once more, it is coming into the print with a considerably favorable setup, as shares have been underperforming for a number of months.

Satya Nadella will take middle stage, and I anticipate he’ll achieve doing what Sundar Pichai didn’t do, which is to offer assurance for the market about AI in each the close to and long run.

The entire firm’s key companies are anticipated to keep up or speed up already elevated progress.

Subsequently, I reiterate Microsoft as a Purchase forward of earnings.