Whereas the market continues to march increased, with the S&P 500 repeatedly hitting new all-time highs, there’s a minimum of one subsector of the market that’s tremendously undervalued in comparison with the place its shares have traded traditionally. That will be the power midstream sector.

Even higher, the midstream trade as an entire is in significantly better form at this time in comparison with a decade in the past when the shares in it traded at a lot increased valuations. Let’s check out the dynamics of the trade and a few shares within the sector that look poised to outperform over the following a number of years.

The midstream sector of the power trade

Whereas the businesses within the midstream area are greatest recognized for his or her pipeline belongings, they carry out a wide range of duties within the power advanced. This ranges from gathering crude and pure gasoline on the wellhead to separating the hydrocarbons (akin to processing and fractionation) to offering water supply and disposal (fracking requires a whole lot of water). It additionally manages storage, long-haul transport, advertising, compression, and different providers.

Midstream corporations are likely to favor fee-based contracts, the place they tackle no commodity and assume no unfold threat. And when new initiatives are constructed they usually include take-or-pay provisions, the place the corporate will get paid whether or not its providers are used or not, or minimal quantity commitments (MVCs), the place the midstream firm will get deficiency funds if a buyer doesn’t use all its quantity capability.

Some contracts nonetheless include value parts that allow midstream corporations take part in commodity value upside as effectively, normally on the pure gasoline and pure gasoline liquid (NGL) facet of the enterprise. For instance, with a percentage-of-proceeds contract a midstream firm will promote residue gasoline and/or NGLs into the market on behalf of a producer and retain a proportion of the sale. One other kind of contract are keep-whole preparations, the place pure gasoline processors maintain the NGLs which might be taken out however should substitute them with an equal quantity of gasoline on a BTU foundation. This exposes an organization to modifications within the costs between NGLs and pure gasoline.

The development lately, although, has favored fee-based contracts, which offer these corporations with a whole lot of visibility. And whereas there’s quantity threat, that is normally considerably mitigated by take-or-pay and MVC provisions. Having belongings tied to demand facilities or stronger basins additionally helps reduce threat, as utility energy demand tends to stay robust whereas basins with higher economics have a tendency to carry up higher during times of decrease costs.

In the meantime, with power demand coming from knowledge facilities given the increase in synthetic intelligence (AI), corporations concerned in pure gasoline transport look effectively positioned to profit from the present AI wave. Goldman Sachs lately predicted that knowledge middle energy demand will develop 160% by 2030, which is able to result in 3.3 billion cubic toes per day of latest pure gasoline demand.

Story continues

Utilities might want to spend money on new technology capability, and new pipelines will probably be wanted to help this development. Midstream corporations with well-established methods round locations with low cost pure gasoline provides, such because the Permian and Appalachia, would be the greatest positioned to profit.

Low historic trade valuations

Between 2011 to 2016, midstream corporations on common traded at an enterprise worth (EV)-to-EBITDA (earnings earlier than curiosity, taxes, depreciation, and amortization) a number of of over 13.5 instances. This is without doubt one of the metrics mostly used to worth these corporations, because it takes into consideration their web debt and the depreciation bills related to constructing out pipelines. Immediately, multiples all through the trade are a lot decrease.

The ironic factor is that the businesses within the area are in significantly better form at this time than they have been throughout that interval. Leverage (debt divided by EBITDA) is down considerably inside the trade, whereas distribution protection ratios are up and midstream corporations are usually producing robust free money circulation.

It is usually price noting the power producer (E&Ps) clients of midstream corporations are usually in higher monetary form, serving to cut back buyer threat, and the trade has turned its give attention to free money over beforehand chasing volumes.

Midstream shares set to outperform

Traditionally low valuations mixed with higher monetary well being and robust development stemming from elevated pure gasoline demand from AI units the trade as much as probably return to the valuation ranges these shares noticed again of their heyday.

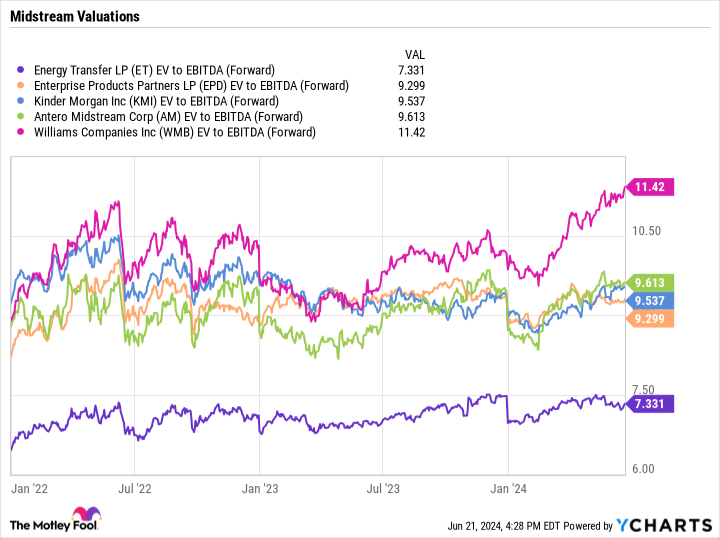

Among the many high shares set to profit are Power Switch (NYSE: ET), Enterprise Product Companions (NYSE: EPD), and Kinder Morgan (NYSE: KMI), all of which have massive built-in methods and robust presences within the Permian. Williams Firms (NYSE: WMB) is one other strong possibility given its massive pure gasoline pipeline system that goes from the Appalachia area to energy demand facilities within the Southeast. Nevertheless, its inventory does commerce at a premium to its friends.

Of the shares highlighted above, Power Switch stands out for its low valuation and development prospects and is my favourite inventory within the area. It and Enterprise even have essentially the most engaging yields of the group at 8.1% and seven.2%, respectively.

A extra under-the-radar identify that would profit is Antero Midstream (NYSE: AM), which has famous how a lot knowledge middle energy consumption demand the Marcellus shale area and its main buyer, Antero Sources (NYSE: AR), have been seeing. Antero Midstream is a well-run pure gasoline gathering operation servicing Antero. It’s benefiting from rebate roll-offs (it beforehand gave Antero Sources a value rebate when pure gasoline pries have been low) and appears poised to begin growing its distribution sooner or later.

Power Switch, Enterprise, Kinder Morgan, and Antero Midstream all commerce at ahead EV/EBITDA multiples of lower than 10, whereas Williams trades at underneath 11.5.

Given the alternatives in entrance of them and the place they commerce at this time versus historic valuations, these undervalued shares may very well be among the many best-performing worth shares over the following a number of years.

Must you make investments $1,000 in Power Switch proper now?

Before you purchase inventory in Power Switch, take into account this:

The Motley Idiot Inventory Advisor analyst group simply recognized what they consider are the 10 greatest shares for traders to purchase now… and Power Switch wasn’t one in all them. The ten shares that made the minimize may produce monster returns within the coming years.

Contemplate when Nvidia made this record on April 15, 2005… if you happen to invested $1,000 on the time of our suggestion, you’d have $723,729!*

Inventory Advisor supplies traders with an easy-to-follow blueprint for fulfillment, together with steerage on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of June 24, 2024

Geoffrey Seiler has positions in Power Switch and Enterprise Merchandise Companions. The Motley Idiot has positions in and recommends Goldman Sachs Group and Kinder Morgan. The Motley Idiot recommends Enterprise Merchandise Companions. The Motley Idiot has a disclosure coverage.

Prediction: These May Be the Greatest-Performing Worth Shares By 2030 was initially printed by The Motley Idiot