Because the Southeast recovers from the devastation introduced by Hurricane Helene, consultants are starting to weigh its results on insurance coverage prices.

Hurricane Helene just isn’t a reinsurance occasion, so it’s unlikely to considerably influence insurance coverage premium charges, in accordance with Mike Chapman, nationwide director of economic markets for HUB Worldwide.

“It is a closely uninsured occasion, so there might be huge financial losses, Chapman informed Business Property Government, “however much less so on the insured aspect.”

Moody’s Analytics estimates Hurricane Helene’s whole property harm at between $15 billion and $26 billion, a quantity that might be additional refined to succeed in an business loss estimate.

READ ALSO: Why Resilience Methods Are a Should

Chapman stated Helene won’t be calculated into his agency’s 2024 hurricane forecast.

“We nonetheless legitimately have two weeks left, and a few exercise is going on within the Atlantic,” he stated. “We don’t actually give new predictions. We examine precise to what we projected.”

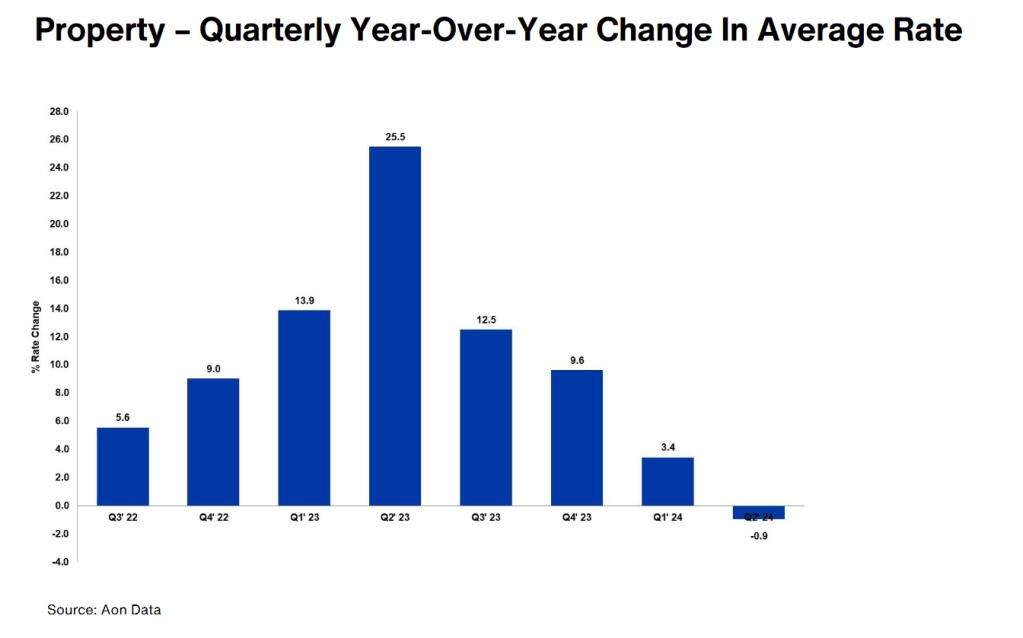

Climbing insurance coverage charges have been way more predictable than most hurricane seasons for industrial actual property house owners and operators. In accordance with a current report from Aon, prices rose for 27 consecutive quarters.

Nevertheless, Aon’s newest property market dynamics report reveals a shift. That streak ended within the second quarter of 2024, because the property year-over-year fee change decreased from +3.4 % within the first quarter to -0.94 % within the second quarter.

Moreover, Aon’s report stated that there’ll proceed to be fee differentiation:

A -10 % to flat fee adjustment for fascinating accounts/occupancies and primarily Nat-Cat uncovered accounts (excluding Florida);

Flat to five % fee will increase for loss-challenged or much less fascinating occupancies;

Flat to 10 % or increased fee will increase for Florida-only accounts or these with important Nat-Cat publicity in Florida.

Vincent Flood, U.S. property apply chief for Aon, stated the charges fell because of shifts in provide and demand.

CRE house owners and operators renew their annual insurance policies all year long, so the timing of the renewal date may have an effect on their renewal charges. Aon stated 70 % of insurance policies are renewed within the first six months of the 12 months, with the second quarter being the busiest and the third quarter seeing the fewest renewal situations.

“In 2023, the insurers have been worthwhile,” Flood stated. “Reductions started in March and have accelerated since.”

The hurricane season ends Nov. 30. Flood stated he’s “cautiously optimistic” that this season might be much less eventful than anticipated. “However we now have an extended method to go,” he added. “Keep in mind, Tremendous Storm Sandy occurred on the finish of October.”

Aon stated it’s too quickly to evaluate Hurricane Helene’s influence.

Some see fee reductions

Patrick McGinley, Vestar president of administration companies, informed CPE that previous to Hurricane Helene, the agency’s annual insurance coverage charges had decreased by over 3 % in comparison with final 12 months.

“By sustaining excessive upkeep requirements and adopting a proactive threat mitigation mindset, we now have efficiently lowered the development of claims over the previous 5 years, which, together with elevated competitors available in the market, allowed for the lower. We’re dedicated to persevering with these practices to make sure a protected and cost-effective surroundings sooner or later.”

Insurance coverage business confronts local weather change extra shortly

Ben Bailey, managing director & head of JLL’s work dynamics insurance coverage enterprise, stated that, operationally, insurance coverage firms are uncovered to the identical extreme climate dangers as many different monetary or skilled service sectors.

“The rising severity and frequency of climate-driven occasions is forcing all industries to bolster their enterprise continuity focus and facility response plans,” he stated.

In accordance with Bailey, what makes insurance coverage distinctive is the publicity firms should claims ensuing from these climate occasions and the corresponding premium changes to cowl these claims. “The truth that insurance coverage firms are being pressured to confront the consequences of local weather change extra shortly than different industries additionally motivates them to deal with proactively managing their very own carbon emissions to keep away from reputational threat,” Bailey stated.

JLL has partnered with a number of throughout the business to develop a baseline for reporting and disclosure functions. In some situations, this helped them formulate a complete portfolio technique to attain their carbon discount targets.

Aon’s report additionally stated shoppers may anticipate an aggressive underwriting strategy for shared and layered accounts with fascinating occupancy lessons and worthwhile historic loss ratios, with or with out heavy Nat-Cat exposures.